Report: Unemployment Headed Over 8% Again

On Friday, financial research firm Lombard Street Research reported that “unemployment could rise above 8% and that profits will be squeezed.”

Lombard Street says its bearish employment and growth projections are the result of a host of factors, including: the 2% payroll tax increase’s drag on retail sales, the ineffectiveness of the Federal Reserve’s monetary pumping, and sequestration—the term used to describe billions in automatic spending cuts set to go into effect March 1st unless Congress acts to change it."Given underlying labor force growth of about 1 percent, this would add 0.7-0.8 percent to the unemployment rate, which was 7.9 percent in January. Even a less pessimistic view of (first quarter) and (second quarter) would send unemployment over 8 percent," said Lombard.

The financial research firm says it predicts the sequester will be shifted to cuts elsewhere but that the reduction in public sector spending will weigh down GDP growth.

"Our assumption is that the sequestration is canceled in favor of further cuts in a new provision. But this means the contribution from public spending to GDP growth could well be more negative than the past -0.4 percent," says Lombard.

The official U.S. unemployment rate is 7.9%. Last quarter, the U.S. economy grew at -0.1%.

Países BRIC: Creciente estatismo y decreciente libertad económica

El crecimiento de este riesgo se puede ver en el siguiente gráfico: el estancamiento de los puntajes de libertad económica de los BRIC según el Índice de Libertad Económica anual elaborado por la Fundación Heritage y el Wall Street Journal.

Como observa Roubini, las “naciones con un mayor desarrollo se arriesgan a anular los logros de la pasada década al aumentar el papel del Estado dentro de la economía”. Roubini informaba de que recientemente los BRIC se han estado alejando de las economías de mercado debido a un incremento de la nacionalización de los recursos, al proteccionismo, a una falta de impulso para realizar reformas estructurales adicionales en pro del mercado que incrementen el tamaño del sector privado y, en general, por el desempeño de un mayor papel por parte del Estado dentro de empresas y bancos. Estas áreas específicas que preocupaban a Roubini se reflejan en los puntajes obtenidos por cada uno de los BRIC en el Índice:

· Brasil. Aunque la

presidenta brasileña Dilma Rousseff ha llegado a un acuerdo para

privatizar algunas compañías que operan autopistas y ferrocarriles

(junto con, quizás, algunos aeropuertos), el gobierno aún domina

demasiados aspectos de la economía del país, minando el desarrollo de un

sector privado más dinámico.

· Rusia. El gobierno del

primer ministro ruso Dmitri Medvédev ha pedido (aunque no las ha puesto

en marcha) reformas de mercado que reduzcan el papel del Estado en la

economía. Sin embargo, estas reformas están siendo obstruidas por la

presidencia de carácter estatista de Putin, así como por las industrias

de propiedad estatal, incluidas las del petróleo, el gas, los oleoductos

y el complejo industrial militar, que se resisten a la transparencia y

la privatización. Además, como según informa el analista de la Fundación

Heritage Ariel Cohen, “Las autoridades policiales y el sistema judicial

rusos son corruptos y se están desmoronando, lo que hace que la

práctica empresarial en Rusia sea doblemente problemática”.

· India. Como informó la

Fundación Heritage el pasado otoño (antes de las nuevas promesas de los

políticos indios de volver a las iniciativas para la reforma del

mercado), el gobierno indio ha sido “tremendamente ineficaz y ha

mostrado señales de un comportamiento depredador, al poner la

recaudación por delante de lo que es mejor para el país. Ha actuado como

barrera en las relaciones económicas bilaterales, por ejemplo, en el

comercio agrícola y en el acceso al mercado financiero. Otras acciones

perjudiciales, como la reciente introducción de un gravamen retroactivo

sobre las empresas multinacionales, desmotivan la participación

extranjera en la economía india en general”.

· China. Aunque China

amplió algunos derechos de la propiedad privada para los granjeros a

finales de los años 70, lo que facilitó un fuerte incremento de la

producción alimentaria y permitió la migración hacia las ciudades que

sustentó la subsiguiente expansión industrial, desde entonces lo avances

en los derechos de la propiedad rural han sido mínimos. Esto es en

parte la causa del intenso deterioro medioambiental y de la caída de los

ingresos en las zonas rurales, muy por debajo de los ingresos en las

zonas urbanas. China es además el “mayor ladrón del mundo” de propiedad

intelectual. Al mismo tiempo, la “OCDE considera las leyes chinas sobre

inversión extranjera como las más restrictivas del G20”. Mientras tanto,

las empresas de propiedad estatal están protagonizando una vuelta a la

escena económica.

Money Is A Form Of Social Control And Most Americans Are Debt Slaves

Michael SnyderEconomic Collapse

Feb 20, 2013

Is America really “the land of the free”? Most people think of money as simply a medium of exchange that makes economic transactions more convenient, but the truth is that it is much more than that. Money is also a form of social control. Just think about it. What did you do this morning? Well, if you are like most Americans, you either got up and went to work (to make money) or to school (to learn the skills that you will need to make money). We spend a great deal of our lives pursuing the almighty dollar, and there are literally millions of laws, rules and regulations about how we earn our money, about how we spend our money and about how much of our money the government gets to take from us. Not that money is a bad thing in itself. Without money, it would be really hard to have a modern society. Unfortunately, our money is based on debt, and debt levels in the United States have exploded to absolutely unprecedented levels in recent years. The borrower is the servant of the lender, and if you are like most Americans, nearly every major purchase that you make in your life is going to involve debt.

Do you want to get a college education so that you can get a “good job”? You are told to get a student loan. Do you want a car? You are encouraged to get an auto loan and to stretch out the payments for as long as possible. Do you want a home? You are probably going to end up with a big fat mortgage. And of course I could go on and on and on. The cold, hard truth of the matter is that most Americans are debt slaves. Most of us spend our entire lives trapped in an endless cycle of debt that we never escape until we die, and meanwhile our years of hard labor are greatly enriching those that own our debts.

Have you ever found yourself wondering why you can never seem to get ahead financially no matter how hard you work?

Well, it is probably because you have gotten yourself enslaved to debt.

Just consider the following example about credit card debt from aformer Goldman Sachs banker…

On the debt side of things, how much does your credit card company earn if you carry just an average of a $5,000 credit card balance, paying, say, 22% annual interest rate (compounding monthly) for the next 10 years?

In your mind you owe a balance of only $5,000, which is not a huge amount, especially for someone gainfully employed. After all, $5,000 is just a quick Disney trip, or a moderately priced ski-trip, or that week in Hawaii. You think to yourself, “how bad could it be?”But a large percentage of Americans never pay off their credit cards at all. They make small payments each month, but then they just keep on adding to their balances.In the end, that is financial suicide.

The answer, including the cost of monthly compounding, is $44,235, or about 9 times what it appears to cost you at face value.

If you carry an “average balance” on your credit cards each month, and those credit cards have an “average” interest rate, you could end up paying millions of dollars to the credit card companies by the end of your life…

Let’s say you are an average American household, and you carry an average balance of $15,956 in credit card debt.Sadly, approximately 46% of all Americans carry a credit card balance from month to month.

Also, as an average American household, let’s assume you pay an average current rate of 12.83%.

Finally, let’s assume you carry this average balance for 40 years, between ages 25 and 65. How much did your credit card company make off of you and your extreme averageness?

Answer: $2,629,618.64

How stupid can we be as a nation?

When you become enslaved to the credit card companies, your toil and sweat makes them much wealthier. It is a form of slavery that does not require anyone pointing a gun at you.

But we never seem to learn. Incredibly, 43 percent of all American families spend more than they earn each year.

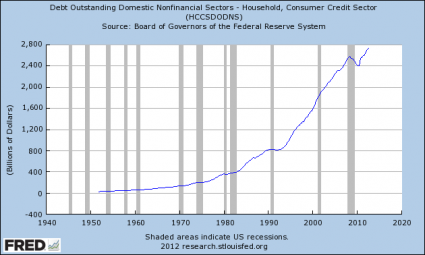

As the chart below demonstrates, consumer credit actually declined for a short while during the last recession, but now it has turned around and the growth of consumer credit is on the same trajectory as it was before the last economic crisis…

Today, the total amount of consumer credit in the United States is 15 times larger than it was 40 years ago.

And every major “milestone” in our lives typically involves even more debt.

-The total amount of student loan debt in the United States recently passed a trillion dollars, and approximately two-thirds of all college students graduate with student loan debt at this point.

-Total home mortgage debt in the United States is now about 5 times larger than it was just 20 years ago, and mortgage debt as a percentage of GDP has more than tripled since 1955.

-Car loans just keep getting longer and longer, and approximately 70 percent of all car purchases in the United States now involve an auto loan.

-Want to get married? That average cost of a wedding is now $26,989which is probably going to mean even more debt unless you have wealthy parents.

-Do you have a serious medical problem? According to a report published in The American Journal of Medicine, medical bills are a major factor in more than 60 percent of the personal bankruptcies in the United States.

Are you starting to understand why approximately half of all Americans die broke?

And I have not even begun to talk about our collective debts yet.

Government debt is a collective form of debt. You may not have voted for any of the politicians that have been racking up debt in your name, but part of it still belongs to you.

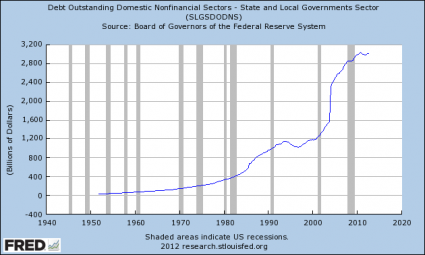

Since the year 2000, state and local government debt has more than doubled. These are collective debts for which we are all responsible…

And of course the biggest collective debt of all is the U.S. national debt. CONTINUE READING